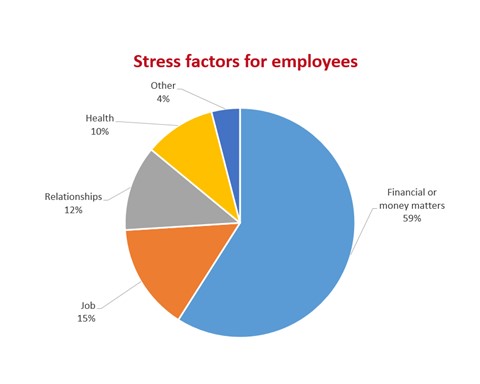

Visualize the situation of an employee thanking his or her stars for having a job in the midst of the COVID-19 crisis. There is a lot of stress from the health crisis all around, given the veritable peril of infection at every step. This is not the only factor bogging the mind of an employee, and the following is an indicative list:

Student loan debt has crossed nearly USD 1.6 trillion in the US alone, as per Wayne Weber, the CEO of Gift of College, a financial services firm that allows employers to contribute to college savings plans and student loan accounts via payments from the payroll.

But how is this related to employees? Simple – many are enrolled for courses to augment their knowledge, and given the financial commitments therein, the stress of loan repayment will continue way beyond the COVID-19 crisis!

Presently, employers can contribute a maximum of USD 5,250 annually, tax-free, toward assistance for current tuition charges, which helps workers who are engaged in studies along with their jobs. However, this does not include the debt already accrued to employees on account of educational debt.

That could change, though, with the coronavirus stimulus package recently announced in the US, offering tax relief for benefits paid out by employers to employees on account of student loan benefits. Passed on March 27, 2020, this is something industry insiders have wanted for a long time. The stimulus bill is for a total of USD 2.2 trillion, and it includes a one-time tax break for annual contributions by employers of up to USD 5,250 per employee, toward the student loan debt of employees.

Why this becomes significant is in view of the trend of many companies – especially the large ones – offering payments for student loans as part of their benefits packages. The International Foundation of Employee Benefit Plans conducted a survey in 2019, as per which out of the 772 organizations who responded,

PricewaterhouseCoopers (PwC), the multinational professional services firm, in 2019 paid USD 25 million on account of student loan debt of its employees. PwC pays USD 1,200 every year for its associates and senior associates for a period of up to six years, to cover their educational loan repayments.

The new provisions allow employers to claim tax relief on account of these educational loan benefits. In 2019, the “Employer Participation in Repayment Act of 2019” bill was introduced, and within it, Section 2206 offers tax relief for payments made in 2020 “by an employer, whether paid to the employee or to a lender, of principal or interest on any qualified education loan incurred by the employee for education of the employee.” This relief is not permanent, however – if it is not renewed, it will expire on January 01, 2021. It could, though, get extended or even made permanent, given how pulling it back could be a risky political maneuver.

The terms of the bill allow employers to put some educational assistance programs in place, covering tax-free educational assistance for employees repaying their education loans as per amounts enumerated above. These payments would not be treated as wages, but would be deducted from taxes on income and payroll from employers and employees.

This is especially helpful given how the workforce is increasingly being burdened with student debt. Estée Lauder, Staples, Sotheby’s, and many other companies have started paying out student loan benefits over the past year. In fact, data from the Society for Human Resource Management (SHRM) indicates that the proportion of employers offering such benefits is up to 8% now, from 4% in 2019.

The benefits also fall to the overall economy. As the world attempts to recover from the shock of COVID-19, this measure will reduce the drag on economic growth, even if for a short period, and help working professionals through the crisis. It could also be an effective tool to get talented employees on board and retain them, allowing smaller companies to compete on more level ground with much larger organizations with more substantial benefits programs.

There is, however, a flip side. The benefit goes only to currently employed professionals, and most employers do not cover student loan payments in their benefits programs. Companies that do offer such programs tend to have employees with higher salaries, implying an advantage only for those in higher income tax brackets. And given how the rewards are more in total compensation for employees with loans than those without, employees may be encouraged to take on loans even if they do not need them, so that these could be paid for by pre-tax dollars or through benefits programs. Student debt could thus rise.

It is also possible that the economic situation in the pandemic may, instead of pushing up the number of employers offering such benefits, actually reduce the numbers. Employers will, after all, look to reduce their costs in their attempt to ride out the crisis. They may want to be more helpful but then their cost pressures are immense!

What is needed, then, is for the provision to be made permanent – or more long-term, at the very least. Also, lawmakers could consider coverage for unemployed personnel with student loans, in addition to those currently working. This could bring true light at the end of the tunnel to professionals looking to ease their education debt burdens.

This website uses cookies to enhance website functionalities and improve your online experience. By browsing this website, you agree to the use of cookies as outlined in our privacy policy .